Credit card search for "new road"

Author:Kuiwen Published Time:2022.09.21

Since September, the pace of banks' credit card debt ABS has been accelerating.

Accelerating the other side, the amount and transaction volume of bank credit card cards have slowed down.

According to the listed bank's interim data, as of the end of June, the cumulative card issuance volume of many banks has slowed down from the end of 2021, mostly below 5%; in terms of transaction volume, many banks have increased year -on -year to negative values.

This is a scene that the bank credit card business has never experienced in the past 30 years. Once upon a time, retail transformation became a consensus of the banking industry, and credit cards were important starting points for retail transformation. Various banks have deployed their horse circles. Now, the growth of this "transformation" is already present. Facing "transformation".

In the future, where does the transformation of credit cards come from? How to find a new direction for development?

New turning: from "quantity" to "quality"

"As early as the 21st century, the 'retail is the future of banks, credit cards are the future of retail', and continued to iterate to the road of retail transformation." The report of Analysys Analysis said that the transformation laid the Merchants Bank towards the "retail of retail sales. The foundation of the king. In 2009, China Merchants Bank opened the "second transformation", and credit cards became one of the three major soldiers of its retail sector.

As the main starting point of bank retail business, credit cards are bidding farewell to the high -speed growth period.

Taking the Retail King's China Merchants Bank as an example, it is experiencing a low speed of credit cards. In the first half of 2022, the credit card circulation card was 105 million, an increase of 2.16%over the end of the previous year. Ping An Bank, a retail dark horse, has developed rapidly in recent years, but the credit card data in the first half of 2022 is not satisfactory. As of the end of June this year, Ping An Bank's credit card circulation card volume was 70.801 million, an increase of 1.0%over the end of the previous year; the total credit card transaction amount of credit cards was 1.79 trillion yuan in the first half of the year, a year -on -year decrease of 1.2%.

In terms of big banks, as of the end of the first half of 2022, ICBC credit card issuance was 164 million, an increase of 0.06%over the end of the previous year; credit card consumption was 1.18 trillion yuan, a year -on -year decrease of 8.53%. CCB credit card has reached 152 million, an increase of 3.29%over the end of the previous year; the consumption transaction value in the first half of the year was 1.44 trillion yuan, a decrease of 4%year -on -year. The transaction volume of the Agricultural Bank of China decreased by 5.90%year -on -year.

In terms of cumulative card issuance, except for Huaxia Bank and Bohai Bank, the cumulative card issuance volume of other national banks is generally lower than 5%compared with the end of the previous year.

After the horse racing circle, the current credit card has formed a relatively stable industry pattern: 7 banks including Industrial and Commercial Bank of China, Construction Bank, Bank of China, China Merchants Bank, and CITIC Bank have accumulated more than 100 million card issuance (Agricultural Bank of China has not announced the cumulative card issuance data, so The data in the mid -term report of 2021 is used as a reference, with a total of 140 million card issuance; the 2021 annual report of Guangfa Bank disclosed the cumulative card issuance of more than 101 million cards), Ping An Bank, Bank of Communications, and other banks issued a total of 50 million to 1 Between 100 million.

However, while the growth of the card issuing cards appears, the credit card is facing bad pressures that have never had before.

The adverse rate rate of China Merchants Bank Credit Card loan was 1.67%, an increase of 0.02 percentage points from the end of the previous year. In addition, the credit card generated 18.048 billion yuan in non -performing loans in the first half of the year, a year -on -year increase of 3.898 billion yuan. The non -performing rate at the end of the first half of the first half

The reporter noticed that on September 20, China Bond Information Network issued the "Explanation and Sales Measures for the Sales and Sales and Sales of the Fourth Period of the Fourth Period of the Fourth Period of Huiyuan 2022", which means that CITIC Bank is allowed to issue 424 million yuan in personal credit card non -performing loans Asset support securities (ABS).

On September 15, China Bond Information Network showed that Pudong Development Bank and China Merchants Bank will issue 483 million yuan and 700 million yuan ABS, respectively. Basic assets are personal credit card non -performing loans. Pudong Development Bank's principal and interest fee for the entry into the pool was 7.764 billion yuan, of which the principal was 6.461 billion yuan; the total principal and interest fee of China Merchants Bank entered the pool was 4.138 billion yuan, of which the total principal was 3.773 billion yuan. On September 9, CCB will issue 485 million yuan ABS; on September 7, Agricultural Bank of China, Bank of Communications, and Guangfa will issue 237 million yuan, 322 million yuan, and 351 million yuan of non -performing credit card claims ABS.

According to incomplete statistics from the China Bond Information Network and Yindeng.com, the Economic Observation Network has found that since this year, many banks have passed the transfer of nearly 90 billion yuan of credit card non -performing assets through the transfer of asset securitization (ABS) and credit asset income rights. For a reference, as of the end of the second quarter of 2022, the total credit card had been overdue for half a year of unpaid credit for 84.285 billion yuan.

A joint -stock bank staff who has been engaged in a credit card direct sales business admits that in previous years, passengers have obtained customers through the Internet line, and the bank has attracted a large number of young customers, but the disadvantages are becoming more and more obvious. On the downward, many banks have to raise the credit threshold. Although many young people applied for credit cards in the first half of this year, there were not many credit cards who could obtain credit by approval. "We want to attract people who record credit records, but usually such people already hold credit cards, and many people even hold multiple credit cards."

To this end, many banks optimize the credit card customer base and asset structure. Xie Yonglin, chairman of Ping An Bank, stated at the bank's 2021 performance conference that in 2021, it began to raise the entry threshold for credit cards and tighten the quota management significantly. "Two years ago, China Merchants Bank optimized the customer structure in terms of credit card business." On August 22, Vice President of China Merchants Bank Wang Jianzhong said at the China Merchants Bank's mid -term performance conference.

"The banking financial institutions shall not directly or indirectly use the number of card issuance, customer quantity, market share, or market ranking as a single or main assessment indicator." At the beginning of July this year, the CBRC and the People's Bank of China jointly released "Notice of Healthy Development" shows that the number of card issues issued by a single customer sets up the number of card issuance, and strengthens the dynamic monitoring and management of sleep credit cards, and strictly controls the proportion.

CITIC Bank Credit Card person said that the credit card business agency will usher in a dense strategic adjustment period. Credit card centers with compliance operations, balanced business structure, and strong customer operating capabilities will be long -term benefits.

"At present, my country's credit card competition pattern has gradually entered the mature stage from the high -speed development stage. The credit card business also faces a breakthrough in transformation. It is necessary to use more standardized business management to seek high -quality development." It is said that with the introduction of the new rules of credit card supervision, the transformation of the industry is imperative. At the same time, during the period when the epidemic and economic downturn, the credit card business, which is closely related to the national consumption, faces more external environmental uncertainty. For the comprehensive operation capabilities of the card issuing, the environmental changes have also forced the environmental change to actively transform the card issuer. Create new development space and business methods.

New direction: Wealth Management

"The customer base has become a compulsory course for the era of stock competition. To do a good job of refined management and personalized refinement in existing customers is the key to retail banks." McKinsey's report shows that the scale growth is no longer the only criterion for success. With the same standard, with the same standard, with the same standard, with the same standard, with the same standard, as the scale is the only criterion, with the same standard, with the same criterion, as the scale is the only criterion, with the same standard, with the same standard, with the same criterion, as the scale is the only criterion. The pace of change has accelerated. While the successful large banks that have successfully occupied the core market in the next 3-5 years, they will also start cross-border competition. Many small institutions can only struggle to survive. Set the upper limit of the number of card issues for a single customer. Strengthen the dynamic monitoring and management of sleep credit cards, and strictly control the proportion.

How to deeply cultivate the group? The strategies of various banks are different.

"Create a full number of personal customer life service platforms." ICBC interim reported to build a full -scale personal customer life service platform. Focusing on the positioning of "life, trust recommendation, points rights, and simplified finance", the construction of ICBC E living platform is comprehensively promoted to provide users with a convenient, efficient and preferential life service experience.

The main source of revenue of bank retail business is asset business, such as loan or credit card installment, and it has begun to turn to wealth management. For example, the China Merchants Bank expands the large customer base and continues to promote the proportion of wealth products in the retail group. As of the end of the first half of this year, the number of retail customers of China Merchants Bank (including debit cards and credit card customers) The number of 40.7486 million households, an increase of 7.84%over the end of the previous year, and 4.0236 million customers in gold sunflower and above, an increase of 9.58%over the end of the previous year.

The transformation of credit cards has also been given a new mission by banks. From consumer finance to wealth management, it has become a new focus of some bank credit card business: using credit cards as banks' entrances, for other businesses, especially wealth management drainage.

Bank of China Merchants Bank, Ping An, CITIC, and Xingye have revealed that the credit card business is breaking through a comprehensive operation, which will strengthen the digital business capabilities of credit card loan products, strengthen the linkage of consumer finance business, wealth management business, basic retail business, deepen customer comprehensive customer comprehensive Management. In the future, credit cards may provide more imagination for leading retail banks comprehensive operations.

In 2021, China Merchants Bank proposed the "Great Wealth Management, Digital Operation and Opening Convergence" 3.0 model. The Merchants Bank semi -annual report shows that the establishment of a large ecology, through business integration, to create a "flywheel effect" that promotes each other and business units, weaving rich ecological scenes for customers. In terms of retail "one -in -one" flywheel, in -depth promotion of the integration of debit cards and credit cards, customer acquisition and integration operations. Among the credit card customers holding 63.25%of the "dual card" customers holding China Merchants Bank's debit cards, an increase of 0.64 percentage points from the end of the previous year to the last year Essence

Ping An Bank made clear that its primary goal was wealth management in the semi -annual report of this year.

"At the young stage of the same customer, we help them solve the actual needs of housing, car purchase, and consumption through consumer financial credit cards. With the accumulation of customer wealth, we provide customers with professional asset allocation services to maintain wealth and value value -added. When customers have family and offspring, we can also provide diversified services such as education, medical care, and wealth inheritance in time. "Xie Yonglin, chairman of Ping An Bank, believes that with the value of credit card holder cardholders, To transport live water, from the perspective of customer perspective to open up the connection cycle of consumer finance and wealth management financial services, banks will present a balanced health and sustainable operation.

"Basic retail to send customers our wealth management today." Said Cai Xinfa, president of Ping An Bank, said.

And CITIC Bank is based on the "new retail" strategy, starting from the credit card color scene, creating a special platform for retail integration wealth management services, and promoting retail customers to wealth customers. CITIC Bank believes that in the era of "new retail", residents 'asset allocation diversified, and gradually transferred to financial assets, and had new demand for asset investment; the net value of financial assets and the public offering trend of residents' investment were clear and accelerated. Customer investment increased increased. New difficulty; the rapid growth of generations and the dual overlapping of population aging, wealth management needs to be transformed from simple asset allocation to the full life cycle management. To this end, CITIC Bank launched a comprehensive operation of personal loan customers, promoted the debit card credit card "dual card fusion", established a credit card customer characteristic wealth management service system, and promoted the integration of unlimited cards and private banks' rights, resources, and teams. In the first half of this year, the wealth management in CITIC Bank's credit card business scenario achieved new breakthroughs. Among them, wealth management sales reached 8.4 billion yuan, an increase of 57%year -on -year.

“未来,中信银行信用卡将加速融入全行'新零售'发展战略,加大集团协同力度,坚定推动'轻型化、数字化、生态化'发展新模式。”中信银行信用卡方面表示,具体而言, On the one hand, starting from the full scene of the credit card business, providing customers with comprehensive financial services, expanding the "life+finance" ecosystem, and giving full play to the important role of the "vanguard" of the bank's retail business; on the other hand In the application of fintech, cutting -edge technical capabilities such as big data, blockchain, and the Internet of Things run through the full journey of products, marketing, risk control, operation and other businesses, and give play to the "pioneer team" role that credit cards are in digital transformation and development. Become a new engine that enables growth.

Industrial Bank also aimed at wealth management. The bank's credit card app "Promoting Life" is for retail customers. It builds high -frequency, easy -to -use and even financial and non -financial life scenarios including cars and house trading, creating unique one -stop living services and financial service platforms. Industrial Bank is strengthening scene links, traffic introduction and ecology, to build online wealth sales platforms, and accelerate the embedded in the promotion of Qian Big shopkeeper, mobile banking, Xingye Life, Promotion Butler, and Banking Platform. Interoperability.

- END -

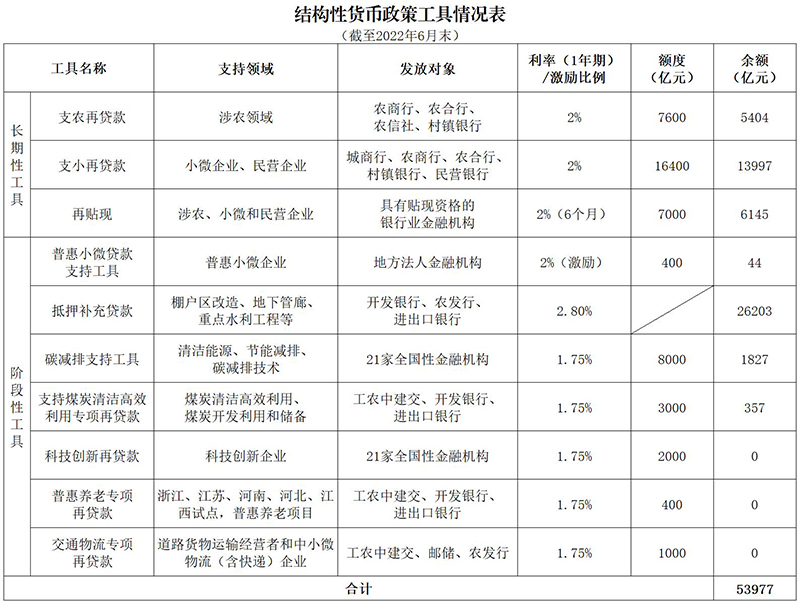

Agriculture, branch small, and multiple special re -loans, the central bank detailed structural monetary policy tools

China Economic Net, Beijing, August 19th. The official website of the People's Ban...

Online information securities have been faked for 6 consecutive years, and they have been fined 430,000 yuan

According to the Red Star Capital Bureau, recently, the China Securities Regulator...